What is GST? It is an indirect tax that hs replaced many indirect taxes in India such as excise duty, VAT, services tax, etc. if you are abusiness man or a person who involve any any kind of selling products you must file GST. and if you are a finance enthusiast, it is very good to understand about GST in detail. In this post GST, its features and importance are explained.

What is GST

GST is known as the Goods and Services Tax. It is an indirect tax that has replaced many indirect taxes in India such as excise duty, VAT, services tax, etc. The Goods and Service Tax Act was passed in Parliament on 29th March 2017 and came into effect on 1st July 2017.

In other words, Goods and Service Tax (GST) is levied on the supply of goods and services. Goods and Services Tax Law in India is a comprehensive, multi-stage, destination-based tax that is levied on every value addition. GST is a single domestic indirect tax law for the entire country.

Also read: GST Return Filing Process-A simple outline

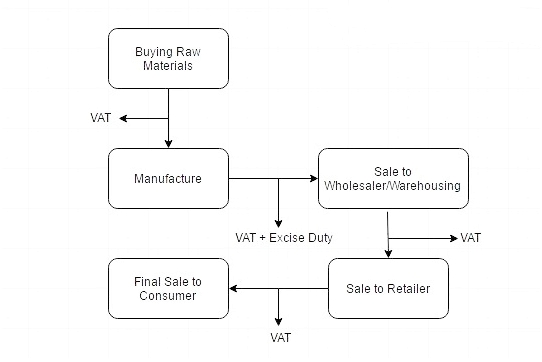

Before the Goods and Services Tax could be introduced, the structure of indirect tax levy in India was as follows:

Under the GST regime, the tax is levied at every point of sale. In the case of intra-state sales, Central GST and State GST are charged. All the inter-state sales are chargeable to the Integrated GST.

Now, let us understand the definition of Goods and Service Tax, as mentioned above, in detail.

Multi-stage

An item goes through multiple change-of-hands along its supply chain: Starting from manufacture until the final sale to the consumer.

Let us consider the following stages:

- Purchase of raw materials

- Production or manufacture

- Warehousing of finished goods

- Selling to wholesalers

- Sale of the product to the retailers

- Selling to the end consumers

The Goods and Services Tax is levied on each of these stages making it a multi-stage tax.

Who should file GST Returns?

GST returns have to be filed by all the business entities who are registered under the GST system. The filing process has to be identified on the basis of the nature of the business.

The registered dealer who is part of the following activities needs to file a GST return:

- Sales

- Purchase

- Output Goods and services tax (on Sales)

- Input Tax Credit with GST paid on the purchase

Value addition

A manufacturer who makes biscuits buys flour, sugar and other material. The value of the inputs increases when the sugar and flour are mixed and baked into biscuits.

The manufacturer then sells these biscuits to the warehousing agent who packs large quantities of biscuits in cartons and labels them. This is another addition of value to the biscuits. After this, the warehousing agent sells it to the retailer.

The retailer packages the biscuits in smaller quantities and invests in the marketing of the biscuits, thus increasing their value. GST is levied on these value additions, i.e. the monetary value added at each stage to achieve the final sale to the end customer.

Destination-Based

Consider goods manufactured in Maharashtra and sold to the final consumer in Karnataka. Since the Goods and Service Tax is levied at the point of consumption, the entire tax revenue will go to Karnataka and not Maharashtra.

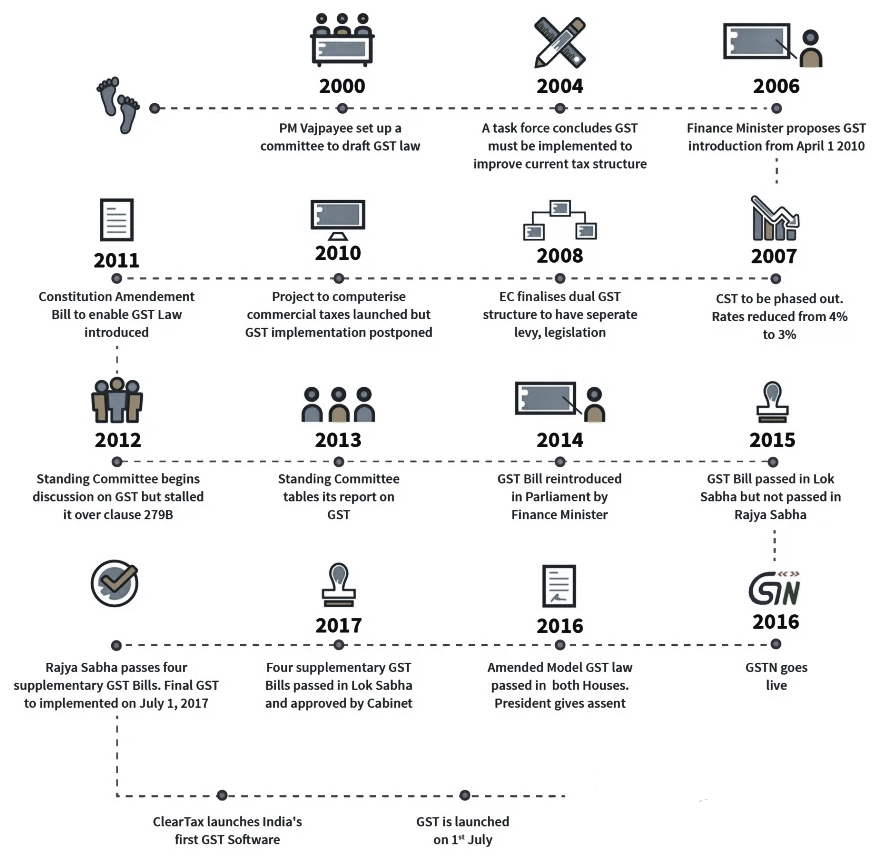

The Journey of GST in India

The GST journey began in the year 2000 when a committee was set up to draft law. It took 17 years from then for the Law to evolve. In 2017, the GST Bill was passed in the Lok Sabha and Rajya Sabha. On 1st July 2017, the GST Law came into force.

Also read: Benefits Of Filing GST Returns On Time

Objectives Of GST

To achieve the ideology of ‘One Nation, One Tax’

GST has replaced multiple indirect taxes, which were existing under the previous tax regime. The advantage of having one single tax means every state follows the same rate for a particular product or service. Tax administration is easier with the Central Government deciding the rates and policies. Common laws can be introduce, such as e-way bills for goods transport and e-invoicing for transaction reporting. Tax compliance is also better as taxpayers are not bogged down with multiple return forms and deadlines. Overall, it’s a unified system of indirect tax compliance.

To subsume a majority of the indirect taxes in India

India had several erstwhile indirect taxes such as service tax, Value Added Tax (VAT), Central Excise, etc., which used to be levied at multiple supply chain stages. Some taxes were govern by the states and some by the Centre. There was no unified and centralised tax on both goods and services. Hence, GST was introduced. Under GST, all the major indirect taxes were subsumed into one. It has greatly reduced the compliance burden on taxpayers and eased tax administration for the government.

To eliminate the cascading effect of taxes

One of the primary objectives of GST was to remove the cascading effect of taxes. Previously, due to different indirect tax laws, taxpayers could not set off the tax credits of one tax against the other. For example, the excise duties paid during manufacture could not be set off against the VAT payable during the sale. This led to a cascading effect of taxes. Under GST, the tax levy is only on the net value added at each stage of the supply chain. This has helped eliminate the cascading effect of taxes and contributed to the seamless flow of input tax credits across both goods and services.

To curb tax evasion

GST laws in India are far more stringent compared to any of the erstwhile indirect tax laws. Under GST, taxpayers can claim an input tax credit only on invoices uploaded by their respective suppliers. This way, the chances of claiming input tax credits on fake invoices are minimal. The introduction of e-invoicing has further reinforced this objective. Also, due to GST being a nationwide tax and having a centralised surveillance system, the clampdown on defaulters is quicker and far more efficient. Hence, GST has curbed tax evasion and minimised tax fraud from taking place to a large extent.

To increase the taxpayer base

GST has helped in widening the tax base in India. Previously, each of the tax laws had a different threshold limit for registration based on turnover. As GST is a consolidated tax levied on both goods and services both, it has increased tax-registered businesses. Besides, the stricter laws surrounding input tax credits have helped bring certain unorganised sectors under the tax net. For example, the construction industry in India.

Online procedures for ease of doing business

Previously, taxpayers faced a lot of hardships dealing with different tax authorities under each tax law. Besides, while return filing was online, most of the assessment and refund procedures took place offline. Now, GST procedures are carry out almost entirely online. Everything is done with a click of a button, from registration to return filing to refunds to e-way bill generation. It has contributed to the overall ease of doing business in India and simplified taxpayer compliance to a massive extent. The government also plans to introduce a centralised portal soon for all indirect tax compliance such as e-invoicing, e-way bills and GST return filing.

An improved logistics and distribution system

A single indirect tax system reduces the need for multiple documentation for the supply of goods. GST minimises transportation cycle times, improves supply chain and turnaround time, and leads to warehouse consolidation, among other benefits. With the e-way bill system under GST, the removal of interstate checkpoints is most beneficial to the sector in improving transit and destination efficiency. Ultimately, it helps in cutting down the high logistics and warehousing costs.

To promote competitive pricing and increase consumption

Introducing GST has also led to an increase in consumption and indirect tax revenues. Due to the cascading effect of taxes under the previous regime, the prices of goods in India were higher than in global markets. Even between states, the lower VAT rates in certain states led to an imbalance of purchases in these states. Having uniform GST rates have contributed to overall competitive pricing across India and on the global front. This has hence increased consumption and led to higher revenues, which has been another important objective achieved.

Advantages Of GST

GST has mainly removed the cascading effect on the sale of goods and services. Removal of the cascading effect has impacted the cost of goods. Since the GST regime eliminates the tax on tax, the cost of goods decreases.

Also, GST is mainly technologically driven. All the activities like registration, return filing, application for refund and response to notice needs to be done online on the GST portal, which accelerates the processes.

- Removing cascading effect on tax.

- Higher threshold for GST registration.

- Composition schemes for small businesses.

- Simpler online facilities for GST compliances.

- Relatively lesser compliances under GST.

- Defined treatment for e-commerce activities.

- Increased efficiency in logistics.

- Regulating the unorganized sectors.

What are the components of GST?

There are three taxes applicable under this system: CGST, SGST & IGST.

- CGST: It is the tax collected by the Central Government on an intra-state sale (e.g., a transaction happening within Maharashtra)

- SGST: It is the tax collected by the state government on an intra-state sale (e.g., a transaction happening within Maharashtra)

- IGST: It is a tax collected by the Central Government for an inter-state sale (e.g., Maharashtra to Tamil Nadu)

In most cases, the tax structure under the new regime will be as follows:

| Transaction | New Regime | Old Regime | Revenue Distribution |

| Sale within the State | CGST + SGST | VAT + Central Excise/Service tax | Revenue will be shared equally between the Centre and the State |

| Sale to another State | IGST | Central Sales Tax + Excise/Service Tax | There will only be one type of tax (central) in case of inter-state sales. The Centre will then share the IGST revenue based on the destination of goods. |

Tax Laws before GST

In the earlier indirect tax regime, there were many indirect taxes levied by both the state and the centre. States mainly collected taxes in the form of Value Added Tax (VAT). Every state had a different set of rules and regulations.

Inter-state sale of goods was taxed by the centre. CST (Central State Tax) was applicable in the case of inter-state sale of goods. The indirect taxes such as the entertainment tax, octroi and local tax were levied together by state and centre. These led to a lot of overlapping of taxes levied by both the state and the centre.

For example, when goods were manufactured and sold, excise duty was charged by the centre. Over and above the excise duty, VAT was also charged by the state. It led to a tax on tax effect, also known as the cascading effect of taxes.

The following is the list of indirect taxes in the pre-GST regime:

- Central Excise Duty

- Duties of Excise

- Additional Duties of Excise

- Additional Duties of Customs

- Special Additional Duty of Customs

- Cess

- State VAT

- Central Sales Tax

- Purchase Tax

- Luxury Tax

- Entertainment Tax

- Entry Tax

- Taxes on advertisements

- Taxes on lotteries, betting, and gambling

CGST, SGST, and IGST have replaced all the above taxes.

However, certain taxes such as the GST levied for the inter-state purchase at a concessional rate of 2% by the issue and utilisation of ‘Form C’ is still prevalent.

It applies to certain non-GST goods such as:

- Petroleum crude;

- High-speed diesel

- Motor spirit (commonly known as petrol);

- Natural gas;

- Aviation turbine fuel; and

- Alcoholic liquor for human consumption.

It applies to the following transactions only:

- Resale

- Use in manufacturing or processing

- Use in certain sectors such as the telecommunication network, mining, the generation or distribution of electricity or any other power sector

What are the New Compliances Under GST?

Apart from the online filing of the GST returns, the GST regime has introduced several new systems along with it.

e-Way Bills

GST introduced a centralised system of waybills by the introduction of “E-way bills”. This system was launched on 1st April 2018 for inter-state movement of goods and on 15th April 2018 for intra-state movement of goods in a staggered manner.

Under the e-way bill system, manufacturers, traders and transporters can generate e-way bills for the goods transported from the place of their origin to their destination on a common portal with ease. Tax authorities are also benefited as this system has reduced time at check -posts and helps reduce tax evasion.

E-invoicing

The e-invoicing system was made applicable from 1st October 2020 for businesses with an annual aggregate turnover of more than Rs.500 crore in any preceding financial years (from 2017-18). Further, from 1st January 2021, this system was extended to those with an annual aggregate turnover of more than Rs.100 crore.

These businesses must obtain a unique invoice reference number for every business-to-business invoice by uploading it on the GSTN’s invoice registration portal. The portal verifies the correctness and genuineness of the invoice. Thereafter, it authorises using the digital signature along with a QR code.

e-Invoicing allows interoperability of invoices and helps reduce data entry errors. It is designed to pass the invoice information directly from the IRP to the GST portal and the e-way bill portal. It will, therefore, eliminate the requirement for manual data entry while filing GSTR-1 and help in the generation of e-way bills too.

Final Thoughts

As we all know GST is an unavoidable part of business. It is an indirect tax that has replaced many indirect taxes in India such as excise duty, VAT, services tax, etc. even we are not dealing with GST, as a finance enthusiast it is good to know about GST. In this post we discussed What is GST and its features and Importance. I hope this post will help you to understand about What is GST and its importance.